In just five years, the CDFI industry has tripled in size to $452 billion. Here’s the data behind that growth

By James Finley

According to a new report released by the Federal Reserve Bank of New York, Community Development Financial Institutions (CDFIs) have grown rapidly in recent years. But as more money flows through the industry, it prompts the question if that growth will translate to support for the communities most in need of CDFIs’ services: minority and low-income communities.

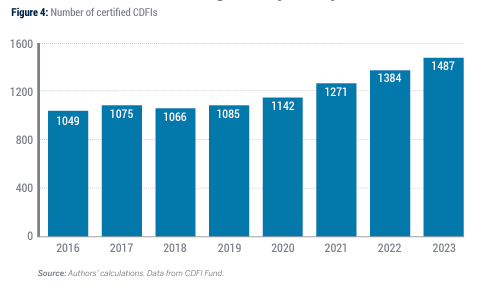

The report, “Sizing the CDFI Market: Understanding Industry Growth,” found that the growth of the industry has been rapid since 2000, but particularly since 2019. In just five years, the CDFI industry has tripled in size to $452 billion, with the number of CDFIs increasing by 40%. However, the report’s authors note that the rise of CDFIs may affect the formation of a secondary market in conflict with the goal of CDFIs.

In theory, the growth of the CDFI industry should serve low- and moderate-income communities. The 1994 Riegle Act, which was created to support CDFIs through the CDFI fund, was focused on addressing challenges faced by Native American communities driven by inequity. As a result, CDFIs were designed to address the needs of low- and moderate-income communities. This originating purpose means that it’s worthwhile to look at the rapid growth of the CDFI industry, and ensure that the industry’s goal remains countering inequity.

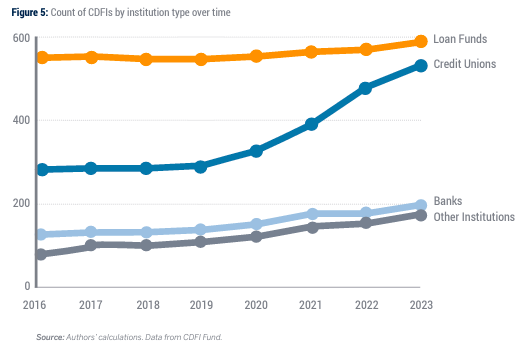

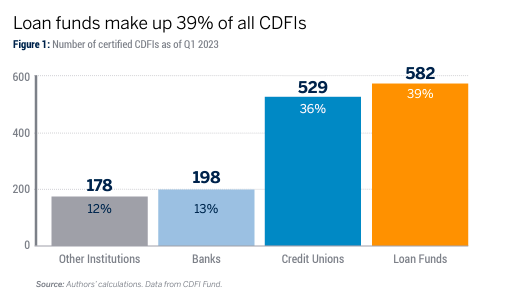

To that end, the report examines the composition of the industry. Since 2019, loan funds and credit unions make up the largest proportion of CDFIs. CDFI credit unions held the plurality of the industry’s assets, at $300 billion, while banks and loan funds held a total of $153 billion. Credit unions were also the fastest growing group, almost doubling to 529 since 2019, substantially increasing their proportion of the market.

The growth of credit unions likely reflects the success of particular organizations that promote CDFIs. Eighty-eight of 239 total credit unions are based in Puerto Rico, which may in large part be attributed to Inclusiv’s Puerto Rico CDFI Initiative’s support converting the island’s existing credit unions, known locally as cooperativas, into certified CDFIS. Many of the members of this network belong to low-income communities, making Puerto Rico a successful application of the CDFI credit union as a regional concept.

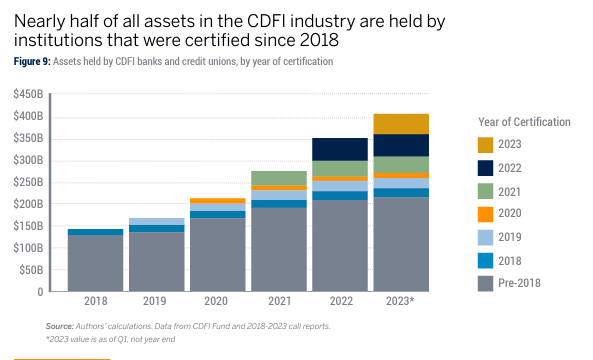

Even beyond the success of Puerto Rico, however, the larger CDFI credit union industry is thriving — approximately tripling to $289 billion — according to the report. This growth comes primarily from entirely new financial institutions: 33% of the industry’s growth since 2018 came from already-certified CDFIs, leaving 67% to come from new CDFIs. These new CDFIs hold nearly half, or $190 billion, of the total assets of the industry.

It’s also important to note that this growth is concentrated in large credit unions. Suncoast Credit Union saw an increase of $7.6 billion and 82%, while First Bank achieved an increase of more than $5 billion and 172%. Institutions on average grew by $3.6 billion and 93%.

As the flow of money has increased in the industry, the study poses a question: Does the industry continue to support the low- and moderate-income communities that they were formed to support? Going forward, the New York Fed’s Community Development team plans to look more closely at the loans provided and sold by CDFIs, to understand how they’ve managed this rapid growth in size in relationship to successfully supporting their original mission.

From the report: “This analysis is the first step in understanding trends in the CDFI industry, including its size and the volume of loan originations, as well as the challenges faced by CDFIs as they serve their target markets and borrowers. In future work, the New York Fed’s Community Development team will examine the origination and sale of various types of loans originated by CDFIs, including residential mortgages, small business loans, commercial real estate and multifamily loans, and secured and unsecured consumer loans.”

This story is part of our series, CDFI Futures, which explores the community development finance industry through the lenses of equity, public policy and inclusive community development. The series is developed in partnership with Next City.